Financial technology or fintech is a burgeoning industry that seeks to make financial systems more efficient and accessible for all users. With the increased demand for faster transactions and greater security, leading-edge technologies like blockchain are gaining fast adoption. Through the use of decentralized networks, blockchain-based fintech apps, also known as decentralized finance or (DeFi) apps, are providing a secure and efficient platform for users to transact.

Financial technology or fintech is a burgeoning industry that seeks to make financial systems more efficient and accessible for all users. With the increased demand for faster transactions and greater security, leading-edge technologies like blockchain are gaining fast adoption. Through the use of decentralized networks, blockchain-based fintech apps, also known as decentralized finance or (DeFi) apps, are providing a secure and efficient platform for users to transact.

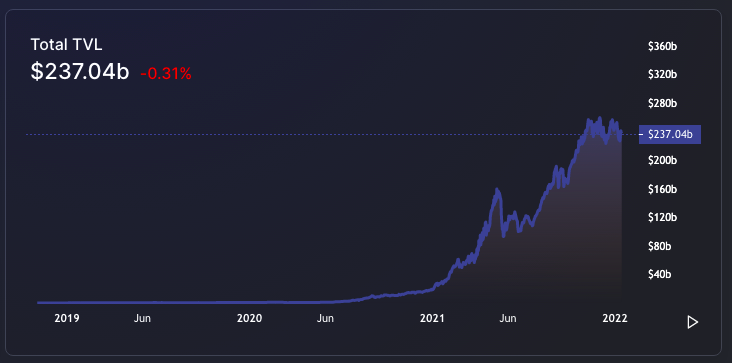

At present, the fintech blockchain market is valued at $6.2 billion and is projected to reach a value of $36 billion by 2028.

In this blog post, we will look into different types of fintech apps that can be developed with blockchain technology and some best practices to follow while designing and developing them.

Types of Fintech Apps Developed with Blockchain Technology

-

DeFi Banking Apps

Decentralized finance (DeFi) banking apps offer users the ability to access a variety of financial services without the need of traditional banking institutions. These apps enable users to store their money in digital wallets, transfer funds between accounts, purchase insurance, and much more.

-

Lending/Borrowing Apps

Blockchain-based lending and borrowing apps allow users to access credit by providing collateral in the form of cryptocurrencies. They also offer a secure platform for peer-to-peer lending, enabling people to borrow money from other individuals without the need for a middleman or credit agency.

-

NFTs Marketplace

Non-Fungible Tokens (NFTs) are unique digital assets that represent ownership of a particular item. NFTs can be used in fintech apps for everything– from trading crypto-collectibles to managing online portfolios. NFT marketplaces enable users to buy and sell these tokens in a secure and transparent manner.

-

Crowdfunding Platforms

Decentralized finance (DeFi) crowdfunding platforms provide a secure way for people to invest in projects they believe in. These apps make it easy for users to participate in fundraising activities without the need for a middleman or expensive transaction fees.

-

Decentralized Crypto Exchange Platform

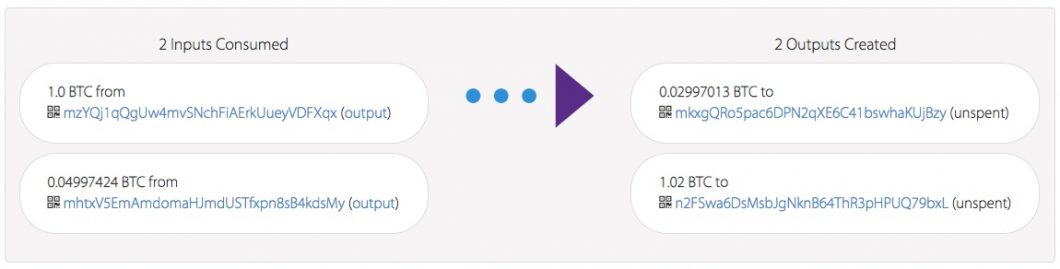

Decentralized crypto exchange platforms allow users to buy and sell cryptocurrencies without the need for a third-party intermediary. These platforms offer secure transaction processing, low fees, and fast settlement times, making them ideal for fintech applications.

Best Practices for Developing Blockchain-Based Fintech App

-

Choose the Type of DeFi App

Before beginning development on a fintech app using blockchain technology, it is important to identify the type and functions of the application required for your business. Conduct diligent market research to understand your competitors, and features trending among DeFi users, and identify features that align with your business. This will help you determine the most suitable blockchain technology stack for your project and minimize future technical debt.

-

Decide Tokenomics

It’s important to consider the tokenomics model of your app before you start developing, as they are an essential part of DeFi applications. Tokenomics is the design principle behind token-based economies. It includes considerations such as incentivizing early adopters of your product, maintaining liquidity in the market, and aligning user motivations with growth.

To offer features such as staking, decentralized exchanges, and liquidity pooling, you will have to introduce crypto tokens along with the mechanism to apply them through your fintech app. For creating an effective token economy, you can leverage tools like OpenZeppelin to ensure the implementation of standard tokens such as ERC721 and ERC20

-

Implement Optimized Development Processes

Developing a successful fintech app requires following a set of best practices for the development process. This includes adapting agile methodologies, test-driven development, continuous integration/delivery, and automated testing. These processes will help ensure that your app is bug-free, meets quality standards, and is ready to deploy.

-

Prioritize Security

While developing a fintech application, security must be the top priority. This means incorporating robust authentication with multi-factor authentication (MFA) and access control measures to protect user data from unauthorized access.

Additionally, developers should utilize encryption for any sensitive information and implement smart contracts for secure transactions. Your developers must be well-versed with different cyber threats such as cross-site scripting, SQL injections, etc, and implement appropriate solutions to mitigate them.

-

Focus on Enriching User Experience

When designing the UX/UI of a fintech app, it is important to keep usability principles in mind in order to create an intuitive and enjoyable experience for users. These principles include things such as simplicity, consistency, visibility, feedback, task orientation, and accessibility. Keeping these principles in mind will help ensure that your app is easy to use while also providing all the features necessary for effective financial management.

-

Develop Scalability Strategies

Building an application with scalability in mind from the outset is key to ensuring its long-term success. Utilizing the right technology stack, understanding capacity planning needs, and implementing performance optimization techniques can all help ensure your app has the capacity to grow over time with minimal downtime.

-

Follow Regulatory Compliance

The financial sector is highly regulated and fintech apps must adhere to the prevailing laws and regulations to run operations smoothly. Developers should always research legal requirements before launching an app and ensure all features comply with necessary standards. This includes considering licensing needs, consumer protection obligations, anti-money laundering and counter-terrorism financing measures, privacy policies, etc.

Conclusion

Developing a successful fintech application requires careful consideration of various aspects such as project scope, technology stack, user experience, scalability needs, and regulatory compliance. By following the right development processes, businesses can create an app that enables users to manage their finances in an intuitive and secure manner.

It’s important to keep in mind that blockchain-based fintech apps require specialized development expertise. At Mindfire Solutions, we have a team of experienced blockchain developers who are well-versed in cutting-edge technologies like blockchain. From creating smart contracts to testing your blockchain-based applications, our end-to-end solution can help you design and develop a top-notch fintech application from the ground up.

Visit Mindfire Solutions to learn more about our services.